When considering whether to take the plunge and invest in property outside of their family home, many question their ability to save a deposit within a reasonable period of time when they already have the commitment of regular repayments on their home loan.

Have you considered that you may not need a deposit? Maybe you are in a better financial position than you think to be able to invest in property. So what do you need to get started?

- equity in your existing home, and

- surplus income to meet the shortfall in expenses after your

tenant’s contribution.

Here’s how it works

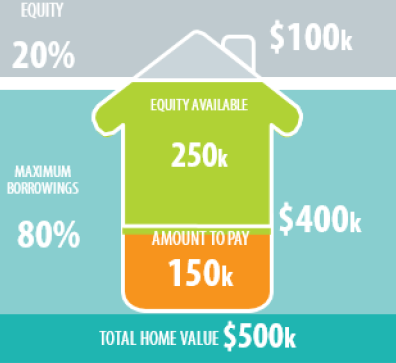

If you already have equity in your existing home or another investment property, you may be able to use your accumulated equity to purchase an additional property. Let’s use an example to explain this process. Your lender will generally allow you to borrow up to 80% of the value of the property (unless you want to pay lenders’ mortgage insurance (LMI)). To keep things simple we will assume that you can only borrow 80%. In our diagram, you have $250,000 in equity in your home that could be used as security to purchase an investment property.

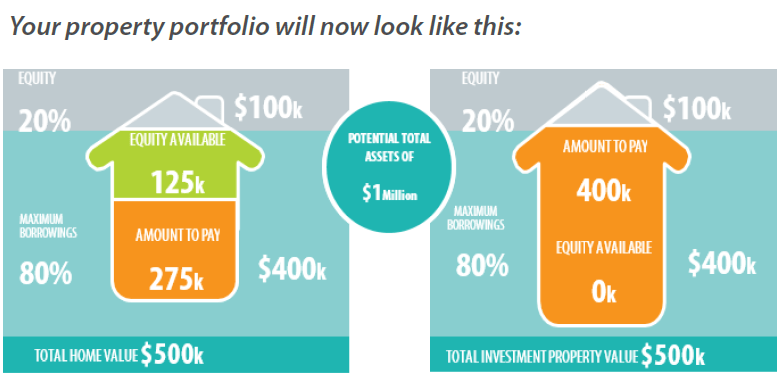

Potential property portfolio

Let’s now assume that you purchase an investment property worth $500,000. You also need to consider the upfront purchase costs. These vary from state to state so we will assume 5% of the total purchase price (or $25,000), resulting in a total cost of $525,000.

You will be able to use 80% of the investment property as security (being $400,000). You will then require an additional $125,000 that can be utilised from your existing home allowing you to borrow the full $525,000 without a deposit.

Adding in $500k for total investment property value, your tenants and the potential to receive a tax refund associated with claiming tax deductions1 for the investment property will help pay for the new loan, however sometimes there could be a shortfall to be serviced. This should be taken into account when borrowing to ensure that the loan on the new investment property and your existing property can be serviced within your budget.

You also need to allow for any unexpected interest rate rises. Then all you need to do is sit back and let the property take its course. Hopefully normal market conditions will deliver capital gains, generating additional equity over time.

Once you learn this strategy you can repeat it as often as you want, provided you can repay the

borrowings.

- Independent financial advice should be sought having regard to

your personal financial circumstances.